How to Choose a Qantas Points Credit Card (Without Overthinking It)

Most people choose a Qantas points credit card based on earn rates. But the real difference comes from how that card fits into your overall points strategy. This guide breaks down high spender cards, low-fee options, and Qantas system maximisers—so you can choose the right card for how you actually spend.

Most people pick a Qantas points credit card by comparing earn rates (or bonus offers).

On the surface, it makes sense.

Higher earn rate = more points.

More bonus points = head start.

But that’s not how strong points strategies are built.

Because a credit card doesn’t exist on its own—it sits inside a broader earning system. And once you understand that system, the role of your card becomes much clearer.

What a Credit Card Actually Does

At a basic level, your card controls two things:

How much of your overall spending earns points for you, and what you earn per dollar at a base level.

That’s it.

It doesn’t create multipliers on its own. It doesn’t optimise where you spend. And it doesn’t guarantee a strong points balance.

Which is why two people with the same card can end up with completely different results.

So let’s have a look at three sets of Qantas points credit cards to help you to get a sense of what is right in a card for you.

High Spender Cards (Built for Volume)

These are the cards most people gravitate toward early when looking for a points-earning card.

They typically come with higher annual fees, higher minimum credit limits, and stronger earn rates—along with higher income requirements to match. In practice, they’re built for people putting meaningful spend through their card each month.

Some examples of Qantas point-earning credit cards in this category are:

NAB Qantas Rewards Signature Card

A solid option if you’re consistently putting through a few thousand per month.

Annual fee: $420 p.a.

Earn rate: 1 Qantas Point per $1 (first $5,000 per statement period), then 0.5 per $1 ($5,001–$20,000)

Spend cap: effectively capped at $20,000 spend per statement period

ANZ Frequent Flyer Black

Very similar positioning, with a slightly higher threshold before the earn rate drops.

Annual fee: $425 p.a.

Earn rate: 1 Qantas Point per $1 (up to $7,500 per statement period), then 0.5 per $1 thereafter

Spend cap: no hard cap, but earn rate reduces beyond the threshold

Westpac Altitude Qantas Black

A solid alternative in the high-spend category, with a slightly lower base earn but a similar structure to NAB and ANZ.

Annual fee: $295 p.a. + $75 Qantas Rewards fee

Earn rate: up to 0.8 Qantas Points per $1 (everyday spend), up to 1.2 per $1 (international spend)

Spend cap: full earn applies up to $10,000 per statement period, then drops to 0.25 per $1

These cards can work well and often come with high introductory bonus offers and a host of other features like lounge passes or travel insurance - but they only make sense if your spending supports them. Otherwise, you’re paying for features and point-earning potential you’re not actually using.

Entry-Level Cards (Simple, Consistent Earning)

This is where most people should start.

These cards are more accessible—lower annual fees, lower income requirements, and simple earn structures. They’re not trying to optimise every dollar. They’re making sure you’re actually earning points across everything.

Some examples in this category are:

Qantas American Express Discovery Card

A clean, no-fee entry point into Qantas points earning. Slightly limited by some merchants not accepting Amex payments.

Annual fee: $0

Earn rate: 0.75 Qantas Points per $1 (everyday spend)

Spend cap: no cap

Bankwest Qantas Platinum Mastercard

Sits slightly higher on fee, but still simple to use consistently.

Annual fee: $199 p.a.

Earn rate: 0.6 Qantas Points per $1 (first $2,500 per month), then 0.3 per $1 thereafter

Spend cap: no cap

Bonus feature: no international transaction fees

Qantas Money Everyday Credit Card

A low-fee, Qantas-linked option that works well if you want simplicity, with a slightly stronger connection into the broader Qantas ecosystem.

Annual fee: $99 p.a.

Earn rate: 0.75 Qantas Points per $1 (up to $3,000 per statement period), then 0.4 per $1 thereafter

Cap: no hard cap on total points, but tiered earn structure acts as a soft cap beyond $3,000/month

Bonus feature: +1 additional point per $1 on Qantas spend

These cards won’t maximise your return and don’t come with the perks of the premium cards. But they solve the more important problem early on:

Finding a way to actually earn points on all of your spending.

And the Qantas Money card has a feature that leads into the next group of cards to highlight.

Qantas Points Maximiser Cards (Where Your Points System Compounds)

This is where things start to scale if you’re deep in the points game.

Some cards don’t just earn points - they earn additional points when your spend runs through Qantas. That includes flights, hotels, wine and most importantly for points-minded people, Qantas Marketplace.

Qantas Money Platinum Credit Card

A strong entry point into Qantas spend-based earning.

Annual fee: $399 p.a. ($349 first year)

Base earn: 1 Qantas Point per $1 (up to $10,000 per statement period), 0.5 thereafter

Cap: no cap on total points earned

Bonus Qantas earn: +1 per $1 on Qantas Spend

Qantas Money Titanium Credit Card

If you’re leaning heavily into Qantas points, this is the heavy hitter, though it comes at a hefty price.

Annual fee: $1,200 p.a.

Base earn: 1.25 Qantas Points per $1 (up to $12,500 per statement period), 0.5 thereafter

Cap: no cap on total points earned

Bonus Qantas earn: +2 per $1 on Qantas Spend

American Express Qantas Ultimate Card

Another big Qantas point earner, though Amex is not as widely accepted by merchants as Visa/MasterCard.

Annual fee: $450 p.a.

Base earn: 1.25 Qantas Points per $1, up to 100,000 Qantas Points in a calendar year, 1 point per $1 thereafter.

Qantas earn: 2.25 per $1 on eligible Qantas spend

Cap: Effectively uncapped, though at a reduced rate beyond 100,000 points.

Bonus feature: $450 a year Qantas travel credit (effectively negating the cost of the card)

Why This Matters

Most people think “Qantas spend” just means flights.

But the real lever is Qantas Marketplace, hotels, wine etc.

Marketplace in particular allows you to purchase gift cards across groceries, retail, dining, and everyday categories at a rate that you wouldn’t otherwise be able to access outside of Woolworths promotions.

So instead of earning 1 point per dollar, you can:

buy a gift card via Marketplace (earning 3+ points per dollar)

pay with your credit card (earning 1-1.5 points per dollar)

trigger bonus Qantas earn (earning another 1-2 points per dollar)

Now you’re creating 5+ points per dollar outcomes on spend that was already going to happen anyway.

And importantly, this is repeatable. It’s not dependent on promotions.

What I Use Personally

At the moment, I use the Qantas Money Titanium Credit Card.

I’m all-in on Qantas points earning, and this card fits the way I structure my spend. Having a card like this is a big part of how I was able to earn nearly 750k points last year and millions over the last few years.

A significant portion of what I spend is routed through Qantas Marketplace so being able to earn both a base rate and an additional 2 points per $1 on Qantas spend makes a meaningful difference over time.

It’s not the right card for everyone. But in a system where you’re deliberately routing spend through Qantas, it becomes a very effective tool.

Where Most People Go Wrong

Most people:

chase the highest earn rate;

ignore how they actually spend;

and don’t think about how their card interacts with Qantas.

That’s how you end up with a premium card… earning average results.

A Simple Example

Someone spending $2,500 per month on a standard card earning 1 point per dollar ends up with around 30,000 points per year.

Run that same spend through a system that incorporates Qantas Marketplace and Qantas spend bonuses, and that number can realistically move into the 60,000–90,000+ range.

Same spend. Different outcome.

Bonus Point Offers (And Why They’re Not the Whole Story)

It’s worth briefly touching on sign-up bonus offers.

These can vary significantly from card to card, and they tend to change frequently—often driven by competition between issuers. At times, they can be very generous and are one of the easiest ways to build a points balance quickly.

That’s especially true if you’re just getting started.

And while they can be valuable, they’re not the full picture.

A strong bonus offer might give you a short-term boost. But your long-term results will still come down to:

how you use your card

where your spending flows

and whether your setup is designed to earn consistently

In other words:

Bonus points can accelerate your balance—but they don’t replace a system.

So by all means, take advantage of a good introductory offer when it makes sense.

Just make sure the card still fits into a setup that works beyond that first bonus.

So, Which Card Should You Choose?

The better question isn’t “what’s the best card?”

It’s:

What role does this card play in my system?

High spend → maximise volume

Starting out → maximise consistency

Optimising → maximise Qantas spend

Because ultimately, the card isn’t the strategy.

It’s the piece that makes the strategy work.

There are great comparison tools available on the Qantas website that you can use to identify which card is best for you, based on the kind of card that you see suiting you and your lifestyle best.

Where to Go Next

If you want to build this properly:

The Starter Kit shows how to structure your everyday spending so more of it earns points.

And The Points Pilot Guides break down how to turn that into a repeatable system that compounds over time.

Want me to build you a personalised points-earnings system so that you’re flying more, for less? Get in touch!

Read some related articles:

How Qantas Points Are Really Earned (On the Ground, Not in the Air)

Most people think Qantas Points are earned in the air. In reality, the biggest balances are built on the ground — through everyday spending, loyalty, and structure. This article explains how the system really works.

Most people assume Qantas Points are earned in the air.

You fly more, you earn more points. Simple.

It’s a logical assumption — and it’s also the reason many people feel like they’re trying to earn points but never quite getting ahead.

The reality is quieter, and a little less exciting:

Most Qantas Points are earned on the ground, in everyday life — not on flights.

Once you understand that, the whole system starts to make a lot more sense.

The Core Misunderstanding

Flights do earn points. But for most people, they’re:

Infrequent

Irregular

Hard to control

You might fly a few times a year. Your everyday spending happens every single day.

That’s where the real leverage is — not because you’re spending more money, but because you’re directing money you already spend more intentionally.

1. How You Spend (Structure Beats Effort)

Everyone already has everyday spending. That part is unavoidable:

Groceries

Fuel

Utilities and household bills

Insurance and subscriptions

Online and in‑store shopping

Where people go wrong is assuming points are earned by adding spending, rather than directing spending that already exists.

In practice, “how you spend” is about asking:

Is my everyday money flowing through channels that actually earn Qantas Points?

When those transactions are aligned with programs that feed into Qantas Frequent Flyer, points start accumulating consistently without changing spending behaviour.

For many Australians, this means everyday ecosystems — things like supermarket rewards programs, fuel partners, and payment methods — quietly doing the work in the background. In the Qantas context, this often includes grocery spend flowing through Woolworths Everyday Rewards, fuel spend flowing through BP Rewards, and everyday payments being made on a Qantas Frequent Flyer–earning credit card.

The same applies to bills and larger recurring expenses. Many people treat these as “points‑dead” categories, even though they represent a significant portion of annual spend — particularly when they’re paid using a points‑earning credit card rather than direct debit or cash.

The key idea here isn’t optimisation or deal‑chasing. It’s intentional routing:

Everyday spend should earn something

Large recurring costs shouldn’t be ignored

Payment methods should support your points goal, not undermine it

When this is set up properly, points are earned quietly, week after week, without conscious effort.

2. Who You’re Loyal To (Loyalty Is Directional)

Loyalty is often misunderstood.

It’s not about liking a brand, chasing specials, or being “locked in”. It’s about where your normal spending is focused.

Everyday spending categories — groceries, fuel, shopping, insurance, travel — always feed into some system, whether you think about it or not. In most cases, unless you consciously do something about it, that system isn’t yours. In those instances, you’re missing out while others are profiting off your spending habits.

The problem most people face isn’t a lack of loyalty. It’s fragmented loyalty.

Many people earn a small number of points across multiple ecosystems:

Some Qantas Points here

Some Velocity Points there

Other rewards scattered across cashback or retailer‑specific programs

On paper, this feels flexible. In practice, it dilutes momentum.

Points strategies work best when there is a clear primary program — a place where the majority of everyday earning is directed.

Concentrating earning toward one frequent flyer ecosystem creates leverage:

Balances grow faster

Redemptions become achievable sooner

Status thresholds (e.g. Points Club) become realistic

This doesn’t mean other programs are “bad” or should never be used.

Woolworths Everyday Rewards and BP Rewards are simply examples of directional loyalty within the Qantas ecosystem. The broader point is not which brands you choose, but that your everyday loyalty consistently feeds into one primary frequent flyer program.

When it comes to points earning, focus beats diversification.

For people aiming to use Qantas Points meaningfully, aligning everyday loyalty around the Qantas ecosystem is far more effective than spreading effort thinly across multiple programs.

3. Connecting the System (Where Most People Lose Value)

This is where everything either compounds — or quietly leaks value.

You can be spending well and loyal to good partners, but still miss out if those decisions don’t connect back to one central system.

Connection is about alignment.

A well‑designed points setup:

Has a clear “home” program (for example, Qantas Frequent Flyer)

Ensures everyday earning feeds back into that program

Avoids unnecessary detours that strand points elsewhere

Without this connection, people often feel like they’re doing the right things, but results stay underwhelming.

Points end up split across programs, trapped below useful thresholds, or expiring before they can be used.

When the system is connected:

Everyday decisions reinforce each other

Points balances build momentum

Promotions and bonuses have something to amplify

This is the difference between earning points occasionally and earning them predictably.

Who This Approach Works Best For

This approach works best for people who:

Have regular everyday spending (groceries, fuel, bills, shopping)

Want to earn points consistently without changing their lifestyle

Prefer clarity and simplicity over juggling multiple rewards programs

Would rather build one meaningful points balance than several small ones

If you fly occasionally — or even frequently — this approach still applies. It simply ensures the time between trips is doing as much work as the trips themselves.

Where Flying Actually Fits In

Flights aren’t irrelevant — they’re just misunderstood.

Flying tends to be the reward trigger, not the main earning engine.

When the ground game is set up properly:

Flights top things up

Status accelerates outcomes

Redemptions become realistic

But without that foundation, flying alone rarely gets people where they want to go.

A Simple Way to Visualise the System

Think of Qantas Points as a flow, not a collection exercise:

Everyday life

Groceries · Fuel · Bills · Shopping

⬇️

Payment & loyalty layer

Rewards programs + Qantas‑earning credit cards

⬇️

Qantas Frequent Flyer

Points accumulate consistently over time

⬇️

Flights & upgrades

The outcome — not the engine

When the flow is clear and aligned, points compound quietly in the background.

The Big Takeaway

Earning Qantas Points isn’t about doing more.

It’s about aligning what you already do so it works together instead of against you.

Get the structure right on the ground, and points stop feeling like something you have to chase.

Flying becomes the bonus — not the plan.

If you want help building this properly, this is exactly what I break down in my guides and consulting. No hype. No hacks. Just a system that actually fits real life.

A Year in Review: Why My Qantas Points Strategy Shifted This Membership Year

This isn’t a points total recap. It’s a look at how my Qantas Points strategy shifted this membership year — away from promo-driven spending and toward a calmer, more repeatable system built around everyday spend.

Most “year in review” posts focus on totals.

Big numbers. Screenshots. Highlights.

This one doesn’t.

Qantas measures behaviour by membership year, not calendar year — and with one month still to go, this isn’t about final outcomes. Instead, it’s about something more useful: how my strategy shifted, and why.

The biggest change this membership year wasn’t earning more points.

It was getting clearer on what should count as everyday spend — and building a system that reflects real life, not just promotions.

When points stop reflecting life, the system breaks

One of the easiest traps in points collecting is letting the earning mechanism dictate spending.

That’s when:

You buy things earlier than you need.

You buy more than you otherwise would.

Points stop being a by-product of life and start driving behaviour.

Over time, that creates friction. It also makes the system fragile — because it only works if you keep forcing decisions.

This membership year, I deliberately stepped back from that.

Why I reduced reliance on Qantas Wine

Wine has historically been a strong points earner for me — and it still can be.

But it’s not a significant part of my everyday lifestyle.

That meant any meaningful volume of wine-related points was coming from:

buying ahead of need;

buying more than I’d otherwise consume (and doing a lot of cellaring); and

spending because of points, not because of life.

This year, I reduced that reliance.

Not because wine offers are bad — they’re often excellent — but because earning points should reflect what you already spend, not what you can be encouraged to buy.

Stepping back from wine made the system:

less capital-intensive;

less promo-dependent; and

more honest.

And, importantly, more sustainable.

Dialling up gift cards — deliberately and precisely

At the same time, I deliberately dialled up gift card usage.

Not as a shortcut.

Not to inflate numbers.

But as a precision tool.

Gift cards weren’t about spending more — they were about extracting more value from spend that was already happening.

Used properly, they:

route everyday purchases through higher-earning channels;

allow stacking without changing behaviour; and

turn neutral spend into strategic spend.

This wasn’t blanket buying or speculative stockpiling. It was:

specific retailers;

clear use cases; and

purchased when the numbers made sense.

That distinction matters. Gift cards are powerful because they amplify existing spend — not because they create new spend.

Insurance: timing matters, but it’s not repeatable

Insurance played a role this year, but it’s worth being clear about how.

The points earned here came from timing a policy review to coincide with a promotion. That’s not something you repeat every year, and it’s not something you should force.

Insurance decisions should always be driven by:

coverage;

cost; and

suitability.

Points are secondary.

That said, if you’re already reviewing a policy, aligning timing with a strong Qantas offer can deliver outsized value. It’s not a core system — it’s a lever you pull when the timing is right.

What didn’t change: cards, structure, restraint

One of the quieter shifts this year was actually not changing much.

My card setup remained largely the same. My Qantas Titanium credit card is the workhorse of the points-earning system and changing it for another card wouldn’t make sense at this point.

There was no constant churn.

No weekly adjustments and time-consuming planning.

Once a structure is right, the goal isn’t activity — it’s consistency.

Letting systems run without interference is often the most underrated skill in points earning.

How the earning mix changed

Looking at where points come from — not just how many — tells a much clearer story about strategy.

It highlights whether points are being earned from everyday behaviour, or from discretionary spending driven by promotions.

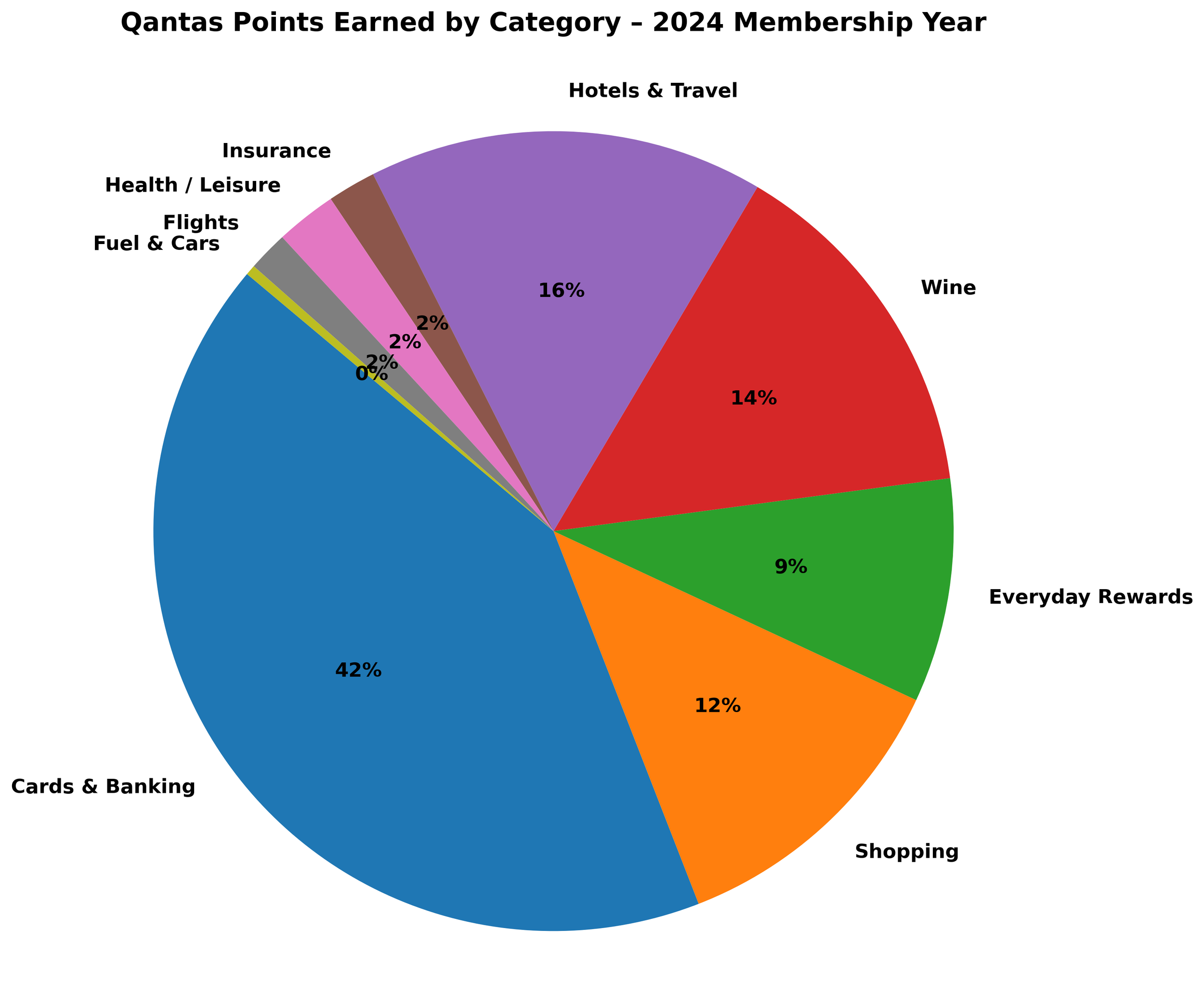

2024 Membership Year

A meaningful share of points came from categories that were not part of my everyday lifestyle, contributing to a more episodic and promo-driven earning profile.

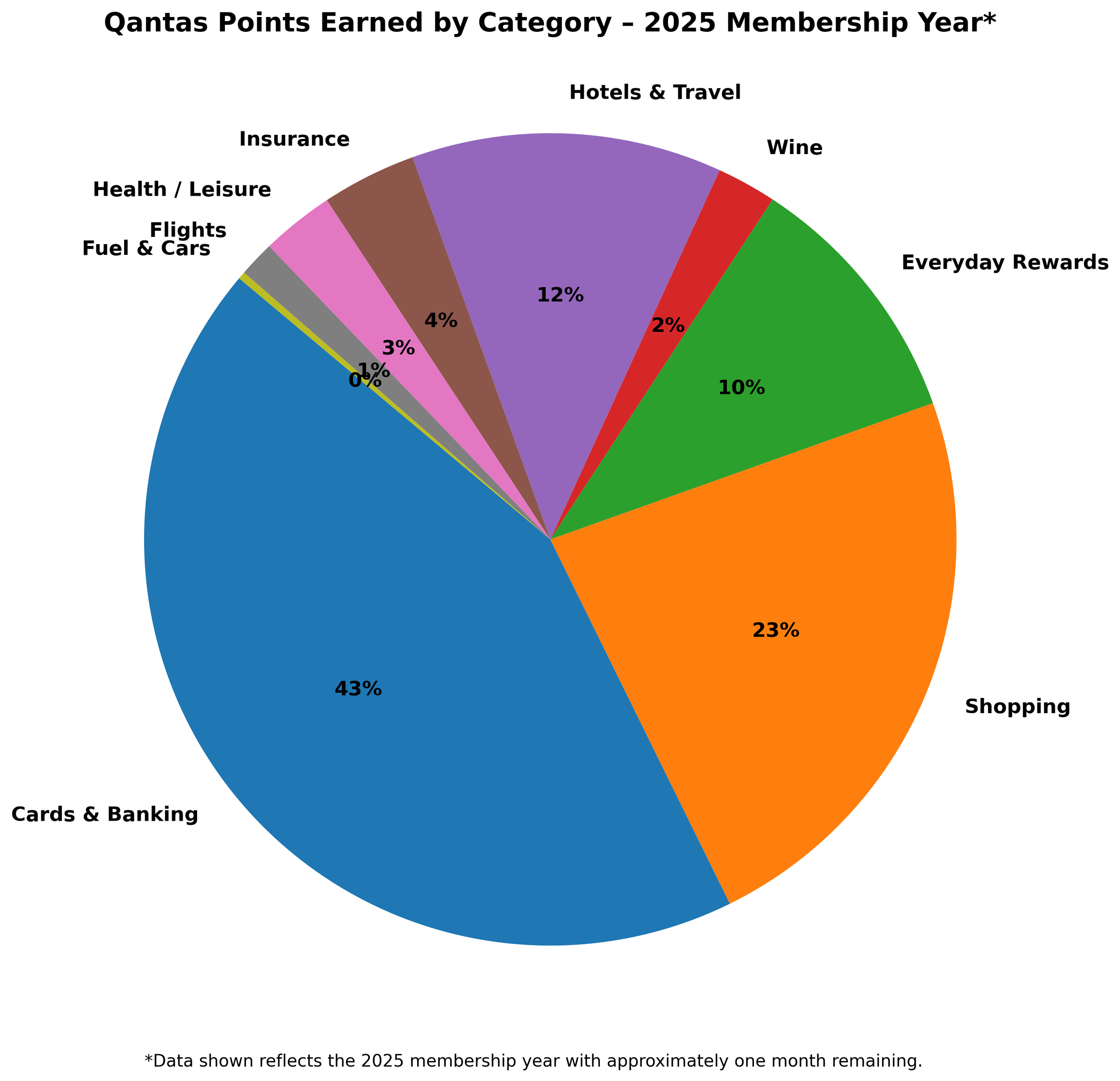

2025 Membership Year

The profile shifted toward genuinely repeatable earning — Everyday Rewards and shopping-led spend — with reduced reliance on non-everyday categories.

Reducing pressure on a single account

Another important shift this year was adding Qantas Business Rewards as a parallel earn stream.

This didn’t inflate my personal Qantas Frequent Flyer results — but it did reduce the pressure to force outcomes into one account.

Separating business-linked earning from personal lifestyle earning made the system calmer and more accurate. Each account now reflects what it’s meant to reflect.

The real outcome: fewer decisions, less noise

The biggest change this membership year wasn’t numerical.

It was psychological.

fewer “should I?” moments;

less urgency around every promotion; and

more confidence letting good offers pass.

The system became quieter — and that’s usually a sign it’s working.

What comes next

At the end of my membership year, I’ll publish a clean, side-by-side comparison — measured the way Qantas actually tracks behaviour.

Not to prove anything.

But to show what happens when points strategies align with real life instead of competing with it.

For now, this review isn’t about totals.

It’s about building a system you don’t have to fight.